AI debt rush meets weakening demand in bond markets

Tech giants are borrowing heavily to fund AI infrastructure, but bond investors are asking for more yield as issuance accelerates.

By Daniel Okafor · Business Editor

3 min read

Big technology companies are relying more heavily on bond markets to finance the AI buildout, and investor demand is weakening as that borrowing accelerates. The shift matters because higher debt costs could make already expensive AI infrastructure plans harder to sustain.

Alphabet, Meta, Amazon and Oracle have sold more than $300 billion of bonds since the start of 2025, according to Bloomberg calculations. Those sales have come alongside spending plans that run into the hundreds of billions of dollars a year, as hyperscalers fund data centers, chips and other AI-related infrastructure through a mix of cash flow, stock issuance and debt.

Other AI-linked companies have also tapped credit markets. Nvidia sold $25 billion of bonds last month, its first debt offering of that kind in five years. SpaceX, which became tied to AI through its acquisition of xAI, sold $25 billion of bonds shortly after a record initial public offering that raised $86 billion in equity.

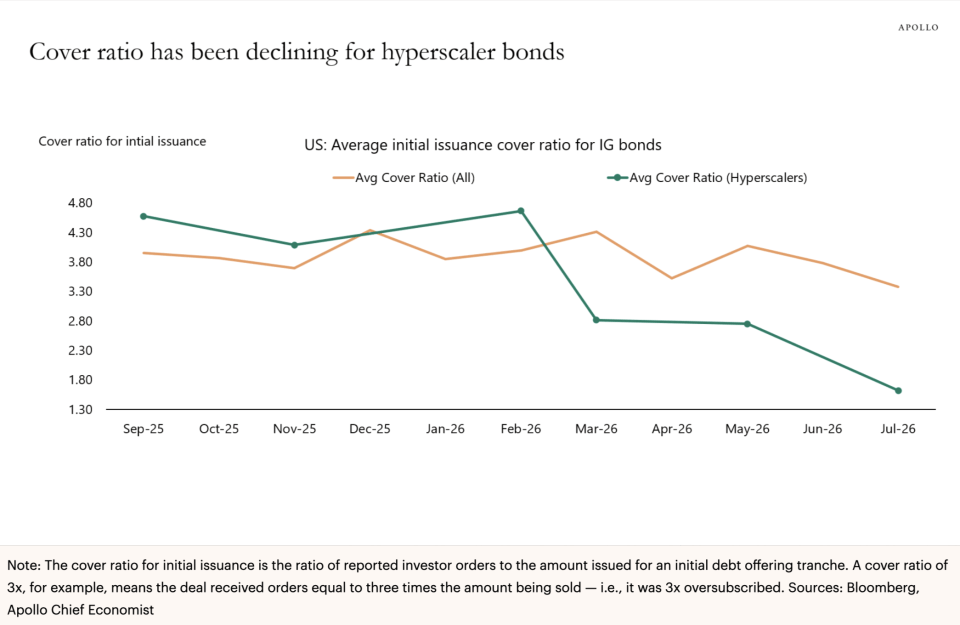

Borrowing needs are set to rise

The debt pipeline is expected to remain heavy. The five largest hyperscalers are projected to sell $300 billion of bonds annually in the coming years, up from $175 billion in 2026, according to the figures cited. JPMorgan estimated SpaceX will receive $375 billion in debt proceeds from 2026 through 2030.

Investors, however, are showing more resistance. Amazon offered an extra 18 to 21 basis points of yield on the longest maturities in a $25 billion bond sale earlier this month after demand softened. Orders amounted to 2.5 times the bonds available, down from 3.2 times in March.

Bank of America wrote in a note that investors were pushing back and said the deal added uncertainty to the supply outlook for hyperscaler and AI-related debt.

Torsten Slok, chief economist at Apollo Global, said in a Wednesday note that cover ratios for hyperscaler bonds have fallen sharply. The ratio, which measures investor orders for each dollar of bonds offered, was close to five times in February 2026 and dropped below two times in July, he said. Slok said that decline suggested investors may demand wider spreads to take on more hyperscaler debt.

The broader investment-grade market has not seen a comparable shift, according to Slok. He said cover ratios for investment-grade bonds overall slipped by about half a point over the same period.

Costs rise as supply builds

The dollar bond market has become crowded enough that some technology issuers have sold debt in other currencies. That pressure means companies may need to offer more favorable terms to buyers, which would raise borrowing costs.

AI-related bonds are also competing with heavy Treasury issuance as the federal deficit grows. The deficit is on pace to reach $2 trillion this fiscal year, according to the figures cited.

JPMorgan strategists wrote Tuesday that the widening in hyperscaler bonds reflects high-grade investors trying to price a faster pace of issuance. Selling pressure has also appeared in the secondary market. SpaceX debt has fallen, pushing yields higher, and is trading at levels similar to junk bonds.

Weakness has extended to equities. SpaceX shares have dropped below their $135 IPO price and are 45% under their peak, which briefly lifted the company’s market value above Microsoft’s. Chip stocks have also been hit, and Nvidia was overtaken by Apple on Friday as the world’s most valuable company.

The latest pressure followed the release of Kimi K3 from Chinese AI startup Moonshot, which said the model beat offerings from OpenAI and Anthropic. Kimi K3 is more expensive than some Chinese rivals but remains far cheaper than leading U.S. models, raising concern that U.S. AI spending plans may face strain if customers adopt lower-cost alternatives.

Citi Research warned Friday that a pullback in AI investment could affect the wider economy because AI-related investment has accounted for more than half of real GDP growth in recent quarters. Citi said a decline could contribute to a mild recession, especially if falling stock prices push consumers to save more and spend less.

This story draws on original reporting from Fortune.